Tin tức

- Nhãn: Thông tin Văn Phòng,

- Tác giả: Admin STS,

- Ngày đăng: 11/01/2026

Triển Vọng Bất Động Sản Thương Mại Việt Nam Q1.2026

Tóm tắt Thị trường

Liên hệ SEE THE SPACE để nhận báo cáo thị trường 2026 và tư vấn thuê văn phòng, kho & khu công nghiệp phù hợp – 100% miễn phí cho khách thuê.

Văn phòng – Công nghiệp – Logistics

Quý 1 2026 đánh dấu một giai đoạn tái cấu trúc rõ nét của thị trường bất động sản thương mại tại Việt Nam.

Khách thuê đang dịch chuyển trọng tâm từ giá thuê niêm yết sang chất lượng không gian, hiệu quả vận hành, tiêu chuẩn ESG và giá trị đàm phán dài hạn.

Ở cả hai phân khúc văn phòng và công nghiệp, quyết định thuê ngày càng mang tính chiến lược, gắn với khả năng vận hành bền vững, trải nghiệm nhân sự và tối ưu chuỗi cung ứng, thay vì chỉ dựa trên chi phí ngắn hạn.

Trong báo cáo này, SEE THE SPACE đưa ra dự báo và phân tích toàn cảnh thị trường, nhằm hỗ trợ doanh nghiệp lựa chọn thời điểm thuê – khu vực – ngân sách một cách hiệu quả.

- Thị trường Văn phòng TP.HCM

- Kho & Nhà xưởng xây sẵn (Ready-built Factory / Warehouse)

- Đất Công nghiệp - So sánh chiến lược Miền Nam và Miền Bắc

1. Thị trường Văn phòng TP.HCM Q1. 2026

Xu hướng Flight-to-Quality tiếp tục dẫn dắt

Sau giai đoạn điều chỉnh 2023–2024, thị trường văn phòng TP.HCM đã bước vào chu kỳ ổn định hơn và chọn lọc hơn.

📌 Nhận định chính:

Các khu vực ngoài CBD đang ghi nhận dư địa đàm phán tốt hơn, trong khi chất lượng tòa nhà, vận hành và tiện ích ngày càng tiệm cận khu trung tâm.

Xu hướng nổi bật

- Doanh nghiệp ưu tiên văn phòng Grade A và Grade B/B+ chất lượng cao

- Gia tăng yêu cầu về trải nghiệm nhân sự, hình ảnh thương hiệu và ESG

- Net effective rent trở thành yếu tố quyết định, quan trọng hơn giá thuê niêm yết

- Nhu cầu dịch chuyển sang các tòa nhà mới ngoài CBD để tối ưu chi phí dài hạn

Giá thuê dự báo:

- Tăng nhẹ 2–4% YoY

- Chủ nhà linh hoạt hơn về thời gian miễn tiền thuê & fit-out

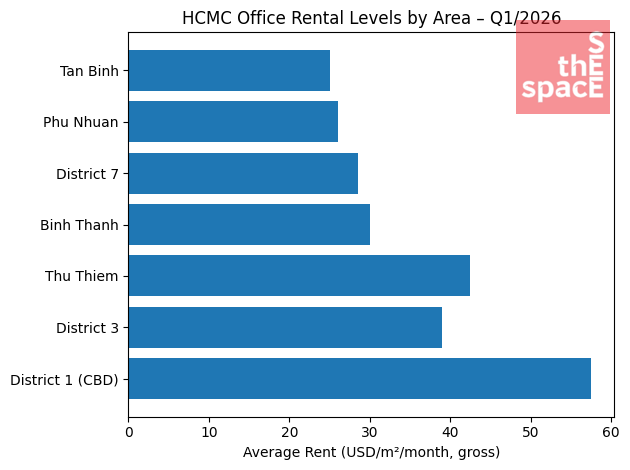

| Khu vực | Phân hạng | Giá thuê (USD/m²/tháng, gross) |

|---|---|---|

| District 1 (CBD) | Grade A | 50 – 65 |

| District 3 | Grade A / B+ | 36 – 42 |

| Thu Thiem | Grade A | 40 – 45 |

| Bình Thạnh | Grade A / B+ | 28 – 32 |

| District 7 | Grade B+ / B | 25 – 32 |

| Phú Nhuận | Grade B+ / B | 24 – 28 |

| Tân Bình | Grade A / B+ | 22 – 28 |

2. Kho & Nhà Xưởng Xây Sẵn

Từ giải pháp ngắn hạn sang chiến lược dài hạn

Đến Q1. 2026, nhà xưởng và kho xây sẵn không còn được xem là giải pháp tạm thời, mà đã trở thành hạ tầng cốt lõi cho các doanh nghiệp logistics và sản xuất.

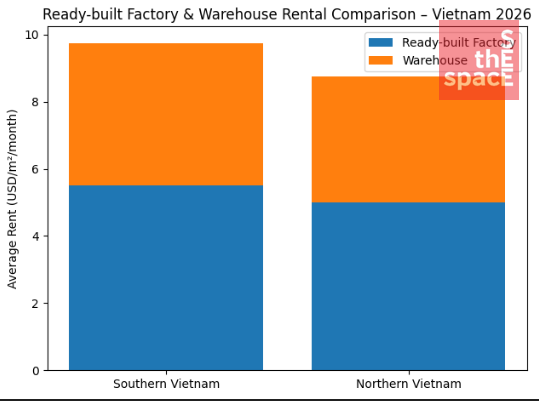

2.1 Giá thuê & đất công nghiệp tham khảo

| Khu tiêu biểu | Ready-built Factory (USD/m²/tháng) | Warehouse (USD/m²/tháng) | Công suất |

|---|---|---|---|

| HCMC – Đồng Nai – Tây Ninh | 4.5 – 6.5 | 3.5 – 5.0 | ~80 – 90% |

| Bắc Ninh – Hưng Yên – Hải Phòng | 4.0 – 6.0 | 3.0 – 4.5 | ~85 – 90% |

2.2 Tổng nguồn cung hiện hữu

- Miền Nam: ~5.5 – 6.4 triệu m²

- Miền Bắc: ~4.5 – 5.1 triệu m²

📌 Phù hợp cho:

- 3PL & logistics

- FMCG & distribution

- Sản xuất điện tử, OEM, xuất khẩu

3. Khu Công Nghiệp Miền Nam vs Miền Bắc Q1.2026: Chọn theo chiến lược, không theo “trend”

Giá đất công nghiệp phụ thuộc vào vị trí, thời hạn thuê còn lại, chất lượng hạ tầng và chính sách ưu đãi từng địa phương.

| Địa bàn tiêu biểu | Vai trò chính | Giá thuê đất KCN (USD/m²/kỳ thuê) | Ngành phù hợp | Ưu điểm chiến lược / Lưu ý cho tenant |

|---|---|---|---|---|

| HCMC – Đồng Nai – Tây Ninh | Trung tâm tiêu dùng & logistics nội địa | 160 – 280 | FMCG, Distribution, Logistics, Sản xuất nội địa | Hệ sinh thái logistics hoàn chỉnh, gần thị trường tiêu dùng lớn; chi phí cao hơn nhưng ổn định, phù hợp chiến lược dài hạn |

| Bắc Ninh – Hưng Yên – Hải Phòng | Trung tâm sản xuất & xuất khẩu | 120 – 200 | Electronics, High-tech Manufacturing, OEM | Chi phí cạnh tranh, kết nối chuỗi cung ứng Trung Quốc & cảng nước sâu; cần đánh giá kỹ lao động & hạ tầng phụ trợ |

📊 So sánh nhanh

- Miền Nam: ổn định, hệ sinh thái hoàn chỉnh

- Miền Bắc: chi phí cạnh tranh, xuất khẩu mạnh

4. Gợi ý chiến lược thuê cho Doanh nghiệp Q1.2026

📌 Q1.2026 là cửa sổ đàm phán tốt nhờ nguồn cung mới và chủ đầu tư linh hoạt hơn.

- Văn phòng: Ưu tiên Grade A ngoài CBD để tối ưu chi phí & trải nghiệm

- Logistics: Ready-built warehouse gần cảng & trục cao tốc

- Manufacturing: Kết hợp đất KCN + nhà xưởng xây sẵn để linh hoạt mở rộng

5. Tư vấn từ SEE THE SPACE

SEE THE SPACE là đơn vị Tenant Advisory độc lập, chuyên:

- Văn phòng

- Kho & nhà xưởng xây sẵn

- Khu công nghiệp

Chúng tôi hỗ trợ:

✔ Phân tích nhu cầu & ngân sách

✔ Shortlist dự án phù hợp

✔ So sánh chi phí thực (Net Effective Rent)

✔ Đàm phán hợp đồng tốt nhất

👉 100% phí tư vấn cho khách thuê = 0

Liên hệ SEE THE SPACE

Để nhận Báo cáo Thị trường 2026 và danh sách Văn phòng / Kho – Nhà xưởng / Khu công nghiệp phù hợp nhất với chiến lược doanh nghiệp:

📞 Hotline: 0768 999 647

📧 Email: leasing@seethespace.vn

🌐 Website: seethespace.vn

Đội ngũ chuyên gia của STS Industrial cam kết cung cấp tư vấn dựa trên dữ liệu, trung lập và tập trung vào hiệu quả triển khai cho khách thuê.

Danh mục

Tin nổi bật

-

Nhà Xưởng Xây Sẵn Cho Thuê 2026: Giải Pháp Công Nghiệp Toàn Diện

Nhà Xưởng Xây Sẵn Cho Thuê 2026: Giải Pháp Công Nghiệp Toàn Diện -

Thuê Văn Phòng Quận 1 l 2026: Giá Thuê, Tỷ Lệ Lấp Đầy

Thuê Văn Phòng Quận 1 l 2026: Giá Thuê, Tỷ Lệ Lấp Đầy -

Thuê Văn Phòng Quận 3 TP.HCM 2026 | Giá Thuê, Hạng Tòa Nhà & Tư Vấn Chi Tiết

Thuê Văn Phòng Quận 3 TP.HCM 2026 | Giá Thuê, Hạng Tòa Nhà & Tư Vấn Chi Tiết -

Thị Trường Văn Phòng TP.HCM 2026: Cơ Hội Vàng Cho Khách Thuê

Thị Trường Văn Phòng TP.HCM 2026: Cơ Hội Vàng Cho Khách Thuê -

Phòng Riêng tại Coworking: Giải PhápTối Ưu 2026

Phòng Riêng tại Coworking: Giải PhápTối Ưu 2026 -

Thành Phố Đồng Nai Ra Mắt 10 Phường Mới: Cơ Hội 2026

Thành Phố Đồng Nai Ra Mắt 10 Phường Mới: Cơ Hội 2026 -

KCN Long An, Bình Dương, Đồng Nai 2026: Tư Vấn Đầu Tư Chi Tiết

KCN Long An, Bình Dương, Đồng Nai 2026: Tư Vấn Đầu Tư Chi Tiết -

Xu Hướng Văn Phòng View Sông Sài Gòn 2026

Xu Hướng Văn Phòng View Sông Sài Gòn 2026 -

Không gian của Bạn, Chuyên gia dẫn lối

Không gian của Bạn, Chuyên gia dẫn lối -

Tư Vấn Coworking TP.HCM cho Doanh Nghiệp

Tư Vấn Coworking TP.HCM cho Doanh Nghiệp